Table of Content

And unlike the deduction for interest on primary mortgages, home equity deductions are disappearing for both new and existing borrowers. In the past, if a taxpayer’s job required certain purchases in order for an employee to perform their job and the employer was unable or unwilling to reimburse the employee, those expenses were tax deductible. For example, employees could deduct mileage driven for work purposes , uniforms, tools, union dues and more as long as they met the 2 percent rule for miscellaneous deductions. BTW, talk with your tax preparer if you prepaid your 2018 property taxes in 2017 in hopes of maxing out your deductions before the tax law change. The rules apply to the return you will file next year, for 2018, said Cari Weston, director of tax practice and ethics for the American Institute of Certified Public Accountants. Interest on home equity loans or lines of credit you paid in 2017 is generally deductible on the return you file this year, regardless of how you used the loan.

We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. Our mission is to protect the rights of individuals and businesses to get the best possible tax resolution with the IRS. You are leaving AARP.org and going to the website of our trusted provider.

The Most Important Real Estate News & Events

The Tax Cuts and Jobs Act of 2017 introduced a slew of new tax breaks while doing away with several others. Some of the tax changes directly affected taxpayers who own a home or plan to purchase one. Under the old rule, taxpayers could claim a child tax credit of $1,000 per child under the age of 17. It then decreased by $50 for every $1,000 a taxpayer earns over specific thresholds.

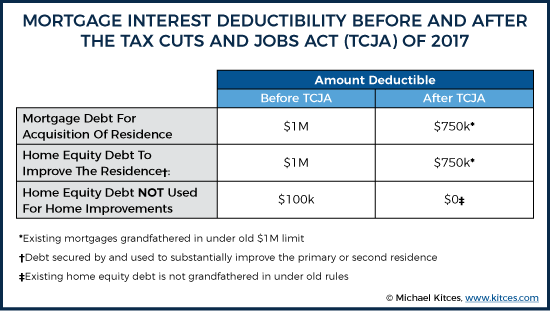

So, starting in 2018, some taxpayers may need to dig out old invoices and create a schedule of expenses to support their mortgage interest deductions. The days of using your home as an ATM and using it to pay off credit card debt — and deducting the interest — are over if you want a tax deduction. Before 2018, you could use cash from these loans to buy a car, pay for college or take a trip, and deduct interest on up to $100,000 of the debt. Two big tax breaks for homeowners were trimmed, leaving many tax filers to no longer have to itemize their tax deductions if they can get a bigger tax break by taking the standard deduction. The TCJA also introduced a cap of $10,000 on itemized deductions for state and local taxes , including property taxes. Homeowners can deduct interest paid on mortgages up to $1 million on a primary home and another qualifying residence.

Is Home Equity Loan Interest Tax-Deductible?

The changes introduced under the TCJA include a reduction of the cap on the mortgage interest deduction. The deduction can be claimed only for the interest paid on mortgage debt up to $750,000 if the loan was taken out after Dec. 15, 2017. A $500 non-refundable tax credit per dependent can also apply to a dependent other than a qualifying child. The credit will begin to phase out for AGI over $400,000 for married couples. Starting in 2018, $750,000 is the maximum amount of debt that can be treated as home acquisition debt for purposes of the mortgage interest deduction. Under the new law interest on home equity debt is no longer deductible.

However, many homeowners will be adversely affected by the TCJA provision that generally disallows interest deductions for home equity loans for 2018 through 2025. This article explains what you need to know to avoid unpleasant surprises when you file your taxes for 2018. Taking the standard deduction would likely give them a bigger tax break than by itemizing. Again, you must choose one or the other — itemizing or the standard deduction — and can’t take both. A way to deduct more than $10,000 — or $5,000 if you’re married filing separately — is if your home is used partially for business or partially rented out.

Increase Your Income and Finish the Year Strong

Rebecca Lake is a journalist with 10+ years of experience reporting on personal finance. This copyrighted material may not be republished without express permission. The information presented here is for general educational purposes only.

If you take out the loan to pay for things like an addition, a new roof or a kitchen renovation, you can still deduct the interest. Many companies understandably collapse under the mountain of debt, including Toys R Us, which eventually went into bankruptcy, closing all its U.S. stores and laying off 30,000 workers without severance. Many PE investors show little interest in the long-term health of the companies they buy or in the welfare of the companies’ workers and communities. Contributed over $33 million during this year’s midterm campaign to the two main GOP congressional super PACs helping elect Republicans to Congress. These groups are effectively controlled by Senate Minority Leader Mitch McConnell (R-KY), who has considerable leverage in the Senate to push for this tax break, and House Minority Leader Kevin McCarthy (R-CA).

They saddle the acquired companies with huge debt and big interest payments, which are then deducted to slash income tax payments. A corporation is limited in the amount of interest it can deduct to 30% of its income, which is calculated narrowly beginning this year. Corporate lobbyists are trying to expand the definition of income so that they can get a much bigger tax deduction.

For homeowners with a mortgage around $300,000 or less, it will probably make more sense to take the standard deduction, says Bryan Gray, a certified public accountant and certified financial planner in Clifton Springs, NY. Mortgageloan.com is a product of ICB Solutions, a division of Neighbors Bank. ICB Solutions partners with a private company, Mortgage Research Center, LLC, (nmls # 1907), that provides mortgage information and connects homebuyers with lenders. Neither Mortgageloan.com, Mortgage Research Center nor ICB Solutions are endorsed by, sponsored by or affiliated with any government agency. ICB Solutions and Mortgage Research Center receive compensation for providing marketing services to a select group of companies involved in helping consumers find, buy or refinance homes. If you submit your information on this site, one or more of these companies will contact you with additional information regarding your request.

Highest rate is applicable to taxable income above $500,000 for single taxpayers and head of household, and $600,000 for married taxpayers filing jointly. So, many taxpayers tapped into their home equity to pay for, say, vacations, college tuition, vehicle purchases and living expenses. And they counted on deducting interest on those loans each tax year. The new rules for deducting interest on home equity loans will put a wrench in those plans, starting in 2018. The good news is not all these changes will apply this upcoming year. On December 2017, President Donald Trump signed the new tax reform law called Tax Cuts and Jobs Act.

By submitting your information you agree Mortgage Research Center can provide your information to one of these companies, who will then contact you. Mortgageloan.com will not charge, seek or accept fees of any kind from you. Mortgage products are not offered directly on the Mortgageloan.com website and if you are connected to a lender through Mortgageloan.com, specific terms and conditions from that lender will apply.

A member of Horizons’ Professional Advisory Circle can help you dig deeper into the laws and help you make wise financial decisions. Estate and gift tax exemption – Effective for decedents dying, and gifts made, in 2018, the estate and gift tax exemption has been increased to roughly $11.2 million ($22.4 million for married couples). National Association of REALTORS® President Elizabeth Mendenhall commended the IRS on its efforts to clarify how homeowners can take advantage of the HELOC tax provision.

Because HELOC loans are secured by real estate, rates on these loans are considerably lower than rates for an unsecured loan. A homeowner scores a lower interest rate and was able to to deduct the interest from their taxes. The new law closes this “loophole” for using home equity as a cheap source of consumer financing. Homeowners previously were able to write off the interest on mortgages up to $1 million. Under the new tax law, however, the cap has been reduced to $750,000 in qualified residence loans.

No comments:

Post a Comment