Table of Content

- For some, interest is still deductible despite the Tax Cuts and Jobs Act

- Home Equity Loans and the Cap on Home Loan Tax Deductions

- How Much Does H&r Block Charge To Do Taxes

- Our mission is to protect the rights of individuals and businesses to get the best possible tax resolution with the IRS.

- How Long to Keep Tax Records and More: A Checklist

- MORE IN Money

- Is There A Best Time Of Day For Therapy? Here's What Therapists Say.

You can obtain relief from these penalties if you can demonstrate that you properly disclosed your tax position in your return and that you had a reasonable basis for taking that position. Photograph of tax forms with miniature house and money, selective focus. Oct 22, 2019 — The Tax Cuts and Jobs Act passed in December 2017 no longer permits an individual to deduct the interest paid on home equity loans. Mar 3, 2022 — Prior to 2018, there were no qualifications on the tax deductibility of interest paid on a home equity loan or HELOC. For a home equity loan, you can deduct the interest on up to $750,000 of the loan.

According to the IRS, interest on home equity loans or home equity lines of credit is not tax deductible if the borrowed amount is not used to buy, build, or substantially improve the home against which the money was borrowed. To get more than your standard deduction, you might need a sizable loan or other expenses to help . If you are on the fence about a property remodel, then borrowing against your home just to take advantage of deducting the interest is probably not your best choice. Taking out a home equity line of credit may still be worth it even if the interest is not deductible to you, depending on how you plan to use the money. If youre interested in consolidating credit card debt, for example, and if you can get a much lower rate with a HELOC, then you could save money this way. Of course, this strategy assumes that youll pay the HELOC down as quickly as possible to minimize interest charges and that you wont run up new debt on the cards that youve paid off.

For some, interest is still deductible despite the Tax Cuts and Jobs Act

If you contribute to a tax-advantaged savings plan, such as an individual retirement account or health savings account, those contributions are still eligible for the same tax benefits. The good news is this change only applies to new homeowners, according to Josh Zimmelman, owner of Westwood Tax & Consulting. The Tax Cuts and Jobs Act, which passed in December 2017, involved some of the most sweeping changes to the U.S. tax system in more than 30 years. And Americans will experience the effects of those changes when they file taxes for 2018.

TaxesFor most tax deductions, you need to keep receipts and documents for at least 3 years. The rules no longer allow you to use home equity loans to get tax-deductible financing for such things as consumer debt and tuition. You just can’t take the interest deduction on the amount used for those purposes, Ms. Weston said. That is because any acquired goodwill and other intangible assets may be written off over 15 years, even if these assets do not lose value.

Home Equity Loans and the Cap on Home Loan Tax Deductions

By submitting your information you agree Mortgage Research Center can provide your information to one of these companies, who will then contact you. Mortgageloan.com will not charge, seek or accept fees of any kind from you. Mortgage products are not offered directly on the Mortgageloan.com website and if you are connected to a lender through Mortgageloan.com, specific terms and conditions from that lender will apply.

All other taxpayers can lose the exemption once they reach $261,500 AGI. The Affordable Care Act used to require both U.S. citizens and non-citizens with a legal residence to have health insurance. Under this rule, people who opted not to buy coverage could face a tax penalty dependent on income.

How Much Does H&r Block Charge To Do Taxes

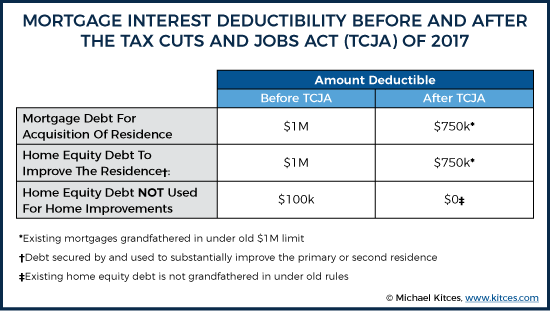

In response, the IRS recently issued a statement clarifying that the interest on home equity loans, home equity lines of credit and second mortgages will, in many cases, remain deductible. Instead, it is classified as home equity debt; so, you can’t treat the interest on that loan as deductible qualified residence interest for 2018 through 2025. The Tax Cuts and Jobs Act changes the rules for deducting interest on home loans. Most homeowners will be unaffected because favorable grandfather provisions will keep the prior-law rules for home acquisition debt in place for them.

The debt was taken out after December 16, 2017 and was used to buy, build, or improve your home, and the total amount of debt throughout 2019 was $750,000 or less. The debt was taken out after October 13, 1987 but before December 16, 2017 and was used to buy, build, or improve your home, and the total amount of debt throughout 2019 was $1 million or less. Casualty losses for such things as a home burglary or a fire are no longer deductible. To claim a casualty loss, the loss has to fall under a presidentially declared disaster, like a hurricane or earthquake. The little-known fact is that you still deduct home equity loan interest in certain circumstances. Private equity managers also often extract excessive fees from their purchased companies.

Our mission is to protect the rights of individuals and businesses to get the best possible tax resolution with the IRS.

As interest on older mortgages retains a legacy to $1 million loans, check carefully with a tax professional about what you can deduct if you have both an older mortgage and a home equity loan that qualifies for deductions. Under the home mortgage interest deduction, home equity loan interest is deductible in certain cases. However, the requirement to use the proceeds for these loans for the home severely limits its potential in 2018 and beyond. The restriction highlights the importance of getting home equity loans and other mortgages only if you need them—not to save money in deductions.

In response to the ambiguity, the Internal Revenue Service recently issued guidance on how to handle deducting interest paid on home equity debt under the new tax law. The IRS clarifies that taxpayers can still deduct interest on home equity loans, lines of credit or second mortgages, regardless of the technical loan label or name, and that it is the use of the loan proceeds that matters. The game-changer, however, is that many homeowners will see a higher tax break by taking the standard deduction, which has doubled to $24,000 for married taxpayers filing jointly. For single filers it’s $12,000, almost double what it was in 2017. So unless your mortgage interest and other itemized deductions total at least that much you're better off just taking the standard deduction. Prior to the recent tax law changes, taxpayers were allowed to deduct qualifying mortgage interest on loans up to $1 million, plus the interest on an additional $100,000 in home equity debt.

Gloria McDonnell is a partner, the tax operations director, and serves on the leadership team at Redpath and Company. She specializes in corporate and individual tax planning and compliance, multi-state taxation, international tax, and tax research. Gloria works with closely-held businesses in a variety of industries, and has provided business tax accounting services since 1989, and has been at Redpath and Company since 1996. This eliminates schemes such as using a sham transaction to save on taxes. For example, you can’t “borrow” from a family member, deduct the interest, and forget about the loan; the loan must function as a true arm’s length transaction.

For example, if a homeowner used a home equity loan to pay off credit card debt, they’d receive a tax break on the interest paid. A refinance is an entirely new mortgage loan involving more stringent credit score requirements, out-of-pocket closing costs and escrow payments. In the past, interest on qualifying home equity debt was deductible regardless of how the loan proceeds were used. A taxpayer could, for example, use the proceeds to pay for medical bills, tuition, vacations, vehicles and other personal expenses and still claim the itemized interest deduction.

The new law imposes a lower dollar limit on mortgages qualifying for the home mortgage interest deduction. Beginning in 2018, taxpayers may only deduct interest on $750,000 of new qualified residence loans ($375,000 for a married taxpayer filing separately). The limits apply to the combined amount of loans used to buy, build or substantially improve the taxpayer’s main home and second home. The confusion stems from language in the new tax law that erased the deduction for home equity debt interest between tax years 2018 and 2026, unless they use the debt to buy, build or improve the home.

No comments:

Post a Comment